What Netflix Gains From a Warner Bros. Deal

Iconic brands, streaming subscribers, and the chance to keep them out of anyone else’s hands.

One of the more striking details in Netflix’s two-decade rise from a US-only DVD-by-mail service to a global entertainment leader is that it built its scale and vast content library without making large acquisitions or competing in Hollywood’s core theatrical movie business. Instead, Netflix’s ascent pushed the rest of the media-entertainment industry into years of merger musical chairs, as companies fought for control of increasingly scarce studio assets (Lions Gate–Starz, AT&T-Time Warner, Viacom–CBS, Disney–21st Century Fox, Amazon–MGM, Discovery–WarnerMedia, Skydance–Paramount).

Now, Netflix has finally found a deal it wants. On January 20, the company agreed to buy the Warner Bros. portion of Warner Bros. Discovery for $72 billion in cash (plus the assumption of debt). If the transaction closes, Netflix will gain control of a century-old film studio, a large catalog of movie and TV content, franchises including Harry Potter and DC Comics, and the HBO brand and its HBO Max streaming platform.

“This is a business and not a religion,” Netflix Co-Chief Executive Ted Sarandos said on a January 20 earnings call, in response to questions about the company’s evolving film strategy and takeover plans. “Conditions change, and insights change.”

Will governments seek to block the deal?

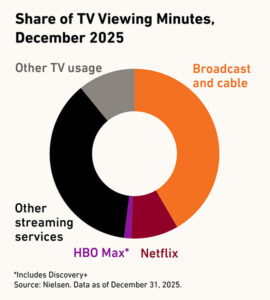

It’s difficult to predict the actions of regulators. Netflix and HBO Max have a 20% and 13% share of the US streaming market, respectively, enough for their combination to potentially raise concerns over market concentration. However, overall TV viewing remains fragmented across various subscription and ad-supported services—including traditional cable, internet-based live programming, and on-demand apps—and the companies’ combined share of total TV usage in minutes will still be small at roughly 10%. Therefore, the resulting change in the broader competitive landscape arguably isn’t significant enough to justify blocking the deal.

Is the deal good for Netflix?

From a financial perspective, the deal offers revenue and cost synergies. Netflix can make better use of Warner Bros.’ intellectual property, investment in which has been constrained by the heavy debt burden of its current parent. On the streaming side, HBO Max is built on dated technology that Netflix will likely upgrade by using its own streaming infrastructure and advertising capabilities.

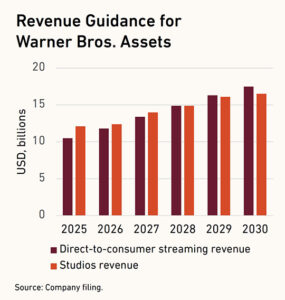

Warner Bros. Discovery’s revenue and adjusted EBITDA projections for the businesses it’s selling (figures that should be taken with a pinch of salt) imply the deal could lift Netflix’s earnings per share 4–5% by 2030. Therefore, the transaction appears accretive but leaves little room for error—or a bidding war. Paramount, backed by David Ellison and his father Larry Ellison, Oracle’s billionaire founder and executive chairman, has made a competing bid to acquire all of Warner Bros. Discovery. While the company rejected the offer, calling it an inferior proposal, it’s unclear whether the Paramount consortium will continue to fight for a deal. At any higher price, Netflix risks overpaying and overextending its balance sheet and should probably walk away in favor of its own content development and other licensing opportunities.

The anticipated M&A costs help explain Netflix’s weaker-than-expected operating margin forecast for 2026; however, the debt-funded nature of the deal may instead shift the market’s focus toward free cash flow, which is estimated to climb 18% this year.

From a strategic perspective, the rationale is strong. Bringing large, potentially under-monetized franchises under Netflix’s control offers a way to broaden its appeal and tighten its grip on subscribers. With DC Comics, for example, Netflix can build its own lucrative superhero franchise to compete with Disney’s Marvel. There is also a defensive element: In light of Paramount’s interest, it makes sense that Netflix would want to keep those assets out of the hands of a rival with deep pockets and strong tech-industry ties. ∎