How to diversify your franked dividends with global equities

Avoiding the risks of an overconcentrated income portfolio.

- The attractive dividends that investors have come to expect from Australian companies are under pressure from a trifecta of separate, and equally menacing, threats:

- High inflation,

- rising interest rates, and

- slowing economic growth.

- Over 80% of dividends paid from Australian companies come from just 4 sectors of the economy, forcing many income-oriented investors to be highly concentrated in industries with significant sustainability challenges.

- The share prices of these companies are exceedingly sensitive to dividend payments, (potentially leaving them under further pressure if dividends falter).

- As interest rates rise and commodity prices fall, rising costs and falling revenues are now squeezing the profits of many Australian companies, which is starting to impact their ability to sustain high dividends.

Many income investors have effectively been forced to choose between appropriately diversifying their equity exposure, and meeting their income requirements with potentially overvalued (and in some cases unsustainable) shareholdings in companies.

- Using its unique structure as an internationally focussed listed investment company, Pengana International Equities Limited (ASX:PIA) shareholders are able to:

- Gain exposure to a professionally managed and diversified portfolio of high-quality and growing global businesses, and

- Receive a fully franked dividend, paid quarterly, which currently equates to a yield of approximately 7.6%1

Notwithstanding bouts of volatility, the Australian economy has remained resilient over recent years, with its equity market delivering solid investment returns in line with its peers.

Dividend yields (on average) now exceed pre-COVID levels, making the market more attractive to income investors, and providing further support to share prices of companies that pay dividends.

But averages can be misleading.

A more detailed analysis reveals that these dividends have become highly concentrated in a few well-performing sectors. This concentration has offset the declining dividends from companies in other sectors of the Australian economy. However, these hot sectors are now showing signs of cooling and dividends are coming under pressure.

The iron-ore price has fallen by more than 20% over the last two months, while coal has seen its price plummet 55% since the start of the year.

Meanwhile, bank lending margins are coming under pressure in Australia (and elsewhere), which leaves the banks’ high dividends more vulnerable.

The Materials sector accounts for 40% of total dividend payments in the Australian ASX All Ordinaries index, up from 28% at the end of 2020. Including financials, real estate and energy sectors brings the total to 80% of total dividends paid in Australia.

Dividends paid from the materials, financials, real estate and energy sectors make up 80% of all Australian equity dividends.

Cyclical industries expand and contract in line with economic cycles. The sustainability of dividends (and share prices) in these sectors is closely linked to the health of the domestic property market, and global demand for commodities.

Property is highly sensitive to interest rates, which have now increased significantly, leading to lower transaction prices, although these have not necessarily been fully reflected in the valuations of unlisted assets. Energy prices – such as LNG and coal – are now falling as the global economy slows. Industrial commodity prices – such as iron ore – are highly sensitive to China’s real estate market and industrial production. These may see slower growth as China’s economy pivots more towards consumption.

Dividend payments by these companies (and hence also by the overall Australian share market) are particularly vulnerable to the downturn in property and energy prices.

Investors who diversify some of this risk by gaining exposure to high-quality innovative companies which are growing earnings across a wider spectrum of the global economy may be well placed to absorb such downturns.

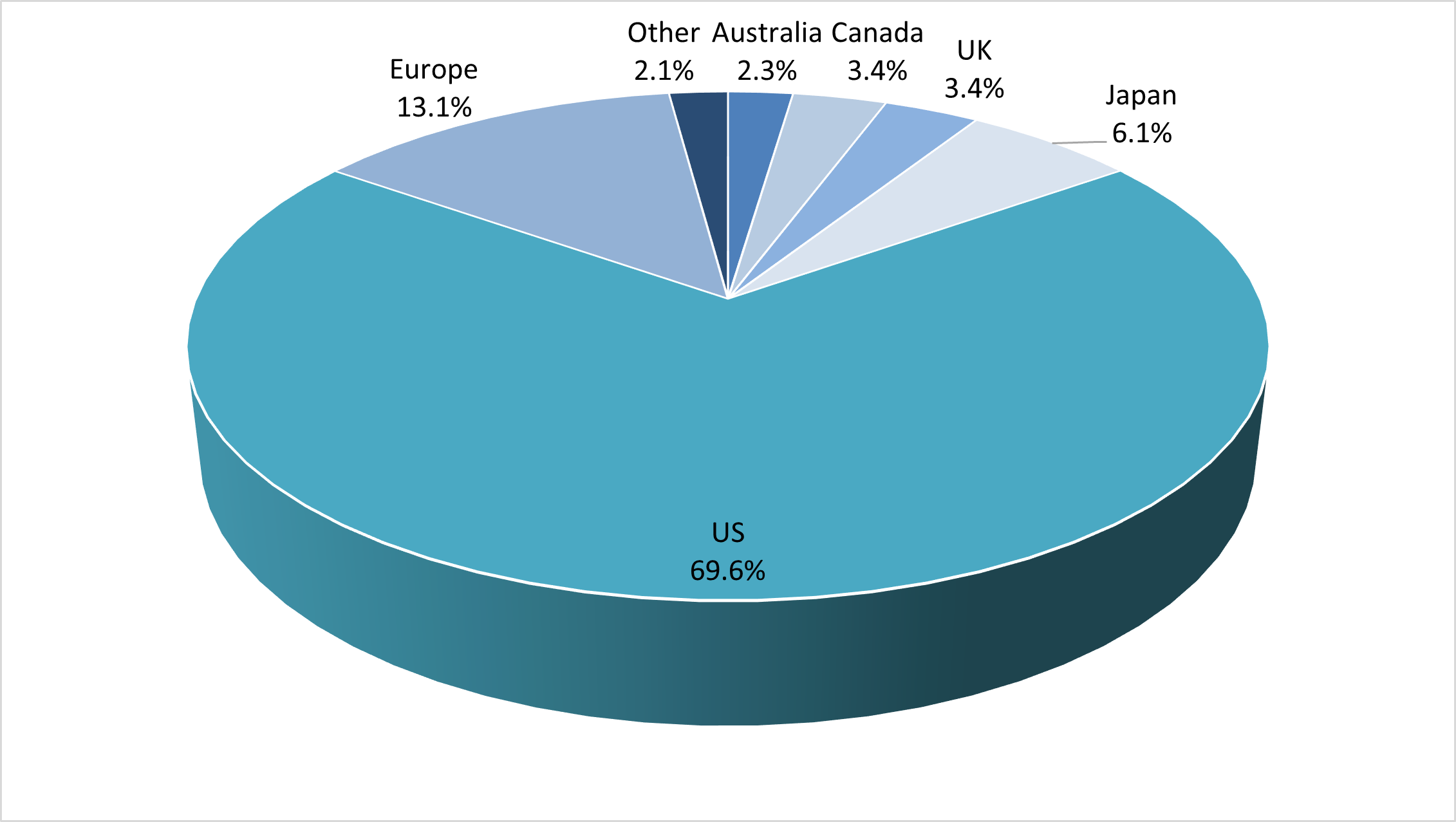

The below chart shows the small scale of the Australian share market compared to the equity universe.

MSCI Global Index by Country 28 February 2023

Source: MSCI

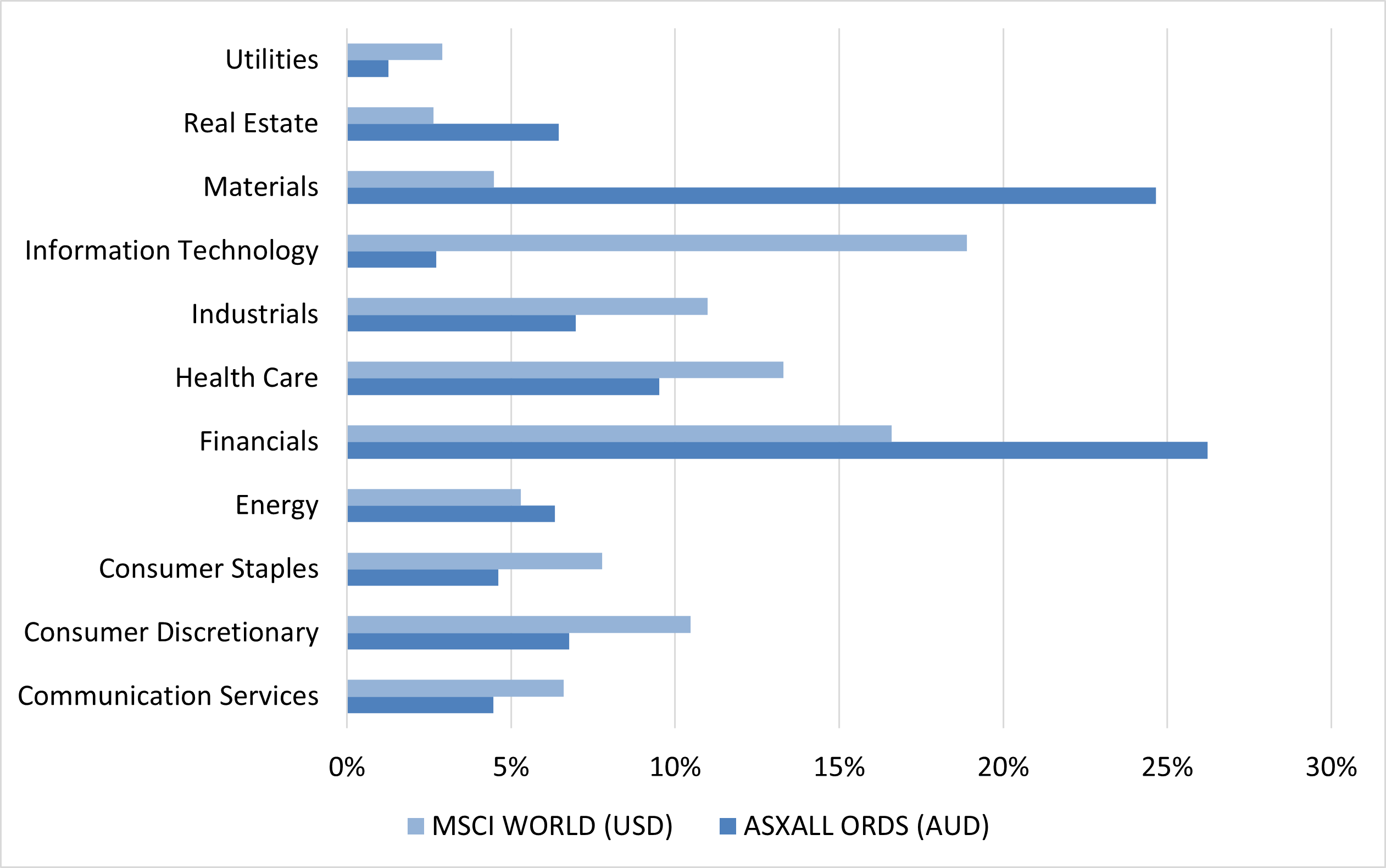

The next chart reveals how benchmark aware investing in the Australian share market brings a highly concentrated portfolio, with more than 50% invested in financials and materials.

It delivers much lower exposure to high-growth companies in the technology and consumer discretionary sectors than are found in the global share market.

Sector breakdown of Australian and Global share markets 28 February 2023

Source: Bloomberg

The final chart illustrates how Australian dividends are even more highly concentrated: 80% of dividend payments in Australia come from materials, financials, real estate, and energy.

ASX All Ordinaries Index – Weighted Dividend Yield – 28 February 2023

Source: Bloomberg

Global equities do not generally pay attractive dividend yields, nor do they generate Australian franking credits. Yield-hungry investors have therefore relied on the Australian share market, and the sectors mentioned above, to deliver an attractive dividend yield.

So how can a Listed Investment Company (“LIC”) structure – as used by ASX listed investment company ‘PIA’ – provide greater sector diversification as well as a franked dividend stream?

The LIC structure of PIA provides the company with more control over the distribution of taxable income compared to traditional unit trusts. This is because there is no requirement to pay out all taxable income to investors at the end of each financial year. This provides a listed investment company the flexibility to smooth dividend payments to investors from year to year.

Importantly, as an Australian company, PIA pays tax on its taxable income, thereby generating franking credits, which can then be passed on to investors when PIA pays its quarterly dividends.

PIA’s global share portfolio is well diversified, typically investing in about 70-80 high-quality growing companies, with overweight positions in the healthcare, technology, and industrial sectors.

As at 30 April 2023, the company already has profit and franking reserves which support a fully franked dividend of 5.4cps per annum, paid quarterly, through to the 31 December 2024 dividend, which is payable in March 2025.

When franking credits are included, this equates to an effective dividend yield of approximately 7.6%1, based on recent share prices.

PIA seeks to invest in high-quality, growing companies in the expectation that they will deliver higher returns, lower risk, and faster growth.

This investment style underperformed last year when energy and resources companies enjoyed higher commodity prices, while lower quality, cyclical businesses benefitted when consumers used savings built up during Covid to keep on spending. However, quality companies that can grow earnings independently of the slowing consumer cycle and high interest rates are now expected to outperform as the economy slows.

For responsible investors, PIA’s portfolio is governed by a robust ethical framework that includes 12 comprehensive negative screens and an ongoing engagement program. This makes PIA the largest international ethical LIC on the ASX.

1 Based on 9 May 2023 closing share price of $0.945, grossed up for franking credits at a 25% company tax rate. Updated yield (based on share price) is available on our company website: www.pengana.com/PIA

This report has been prepared by Pengana Investment Management Ltd (ABN 69 063 081 612, Australian Financial Services Licence No. 219462) (“Pengana”). This report does not contain any investment recommendation or investment advice and has been prepared without taking account of any person’s objectives, financial situation or needs. Therefore, before acting on the information in this report a person should consider the appropriateness of the information, having regard to their objectives, financial situation and needs.

Pengana is the manager for Pengana International Equities Limited (ACN 107 462 966, ASX: PIA) (“PIA”). Pengana has appointed Harding Loevner LP (“Harding Loevner”) as the sub-investment manager for PIA.

None of Pengana, Harding Loevner, nor any of their related entities, directors, partners or officers guarantees the performance of, or the repayment of capital, or income invested in PIA. An investment in PIA is subject to investment risk including a possible delay in repayment and loss of income and principal invested. Past performance is not a reliable indicator of future performance, the value of investments can go up and down.

Pengana has appointed Harding Loevner as Pengana’s corporate authorised representative under Pengana’s AFSL.

While care has been taken in the preparation of this information, neither Pengana nor Harding Loevner make any representation or warranty as to the accuracy, currency or completeness of any statement, data or value. To the maximum extent permitted by law, Pengana and Harding Loevner expressly disclaim any liability which may arise out of the provision to, or use by, any person of this information.

None of Pengana International Equities Limited (“PIA”), Pengana Investment Management Limited (ABN 69 063 081 612, AFSL 219462) nor any of their related entities guarantees the repayment of capital or any particular rate of return from PIA. Performance figures refer to the movement in net assets per share, reversing out the impact of option exercises and payments of dividends, before tax paid or accrued on realised and unrealised gains. Past performance is not a reliable indicator of future performance, the value of investments can go up and down. This document has been prepared by PIA and does not take into account a reader’s investment objectives, particular needs or financial situation. It is general information only and should not be considered investment advice and should not be relied on as an investment recommendation.